Market Quarterly | Q1-2026

The audio version

Each quarter we organize the four key market influences in the order that has been the most impact on the stock market. For this quarter, geopolitical takes first place, followed by inflation, employment and interest rates.

There is a lot to unpack on the geopolitical front, so we’ll leave most of that to the news and political commentators so we can focus on the financial implications. While the global conflicts continue to rage and even expand with the U.S.-led bombing of Iran, how is that impacting inflation, interest rates, employment, and the stock market?

The initial impact has been felt at the gas pump, but the broader consequences may still be unfolding. Countries heavily reliant on oil and gas imports that traverse the Strait of Hormuz have resorted to tapping their strategic petroleum reserves to mitigate the immediate effects of rising oil prices. However, with these reserves nearing depletion, the increased cost of petroleum product inputs in manufacturing is anticipated to drive up the prices of goods and services globally. Notably, containerized freight costs have surged by 42.5% over the past year, suggesting that consumer goods prices are likely to rise in the coming months, potentially leading to higher inflation.

Prior to the U.S. attack on Iran, inflation was gradually declining towards the Federal Reserve’s target of 2%. In January and February, it reached 2.4%. However, there was a sharp reversal in March, with the inflation rate increasing by 38% to an annual rate of 3.3%. This significant rise is likely due to the increase in shipping costs. We will closely monitor this situation as it has far-reaching implications, particularly for interest rates and potentially employment.

On the employment front, unemployment has remained steady at 4.4%. Until March, wages were outpacing inflation. However, the recent surge in inflation to 3.3% has now absorbed all pay increases for the working class. Since the U.S. economy is largely consumer-driven, the loss of discretionary and disposable income is expected to ripple through the economy. Nevertheless, it may not have a significant impact on overall consumption.

Current discretionary consumption, the primary driver of the U.S. economy, is fueled by retirees who have experienced a significant increase in their 401(k) balances over the past few years, surpassing their expectations. This consistent spending pattern appears to be supporting the economy’s fundamental pillars, consequently maintaining low unemployment rates. Consequently, this situation presents a weak argument for the Federal Reserve to lower interest rates in the near term.

We would be remiss to overlook the lessons learned from 1973, when interest rates were slashed to prevent an unavoidable recession. This decision led to relentless inflation that took a decade and very unpopular measures to finally bring under control. The crucial takeaway is that lowering interest rates too soon is extremely risky, and the consequences can be quite severe.

What impact have geopolitical upheavals, rising inflation, and the potential for lower interest rates had on the market?

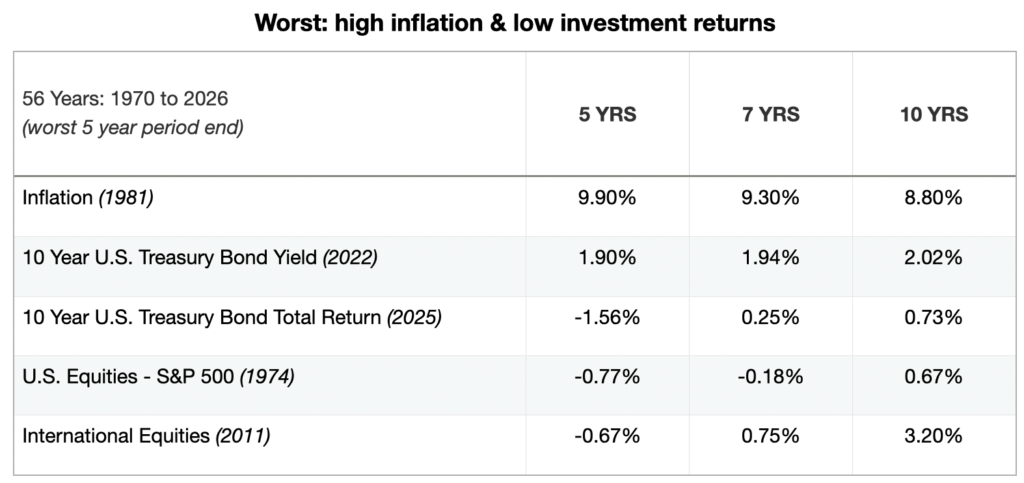

For the quarter ending March 31, the stock market experienced a pullback, and the bond market saw a decline in returns. The U.S. stock market dropped by 1.43%, but over the past twelve months, the S&P 500, which measures the stock market, has returned 17.78%, significantly surpassing the historical average of 12.21% for the past 56 years. Similarly, since 1970, inflation has averaged 4%, exceeding the Federal Reserve’s target of 2%. Consequently, after adjusting for inflation, the stock market has yielded a real return of 8.21%, while U.S. Treasuries have provided a return of 1.96%. While these figures have been highly favorable for investors, it raises concerns for those nearing retirement about the future prospects of the markets. Will the exceptional real returns in excess of inflation continue in the coming decades?

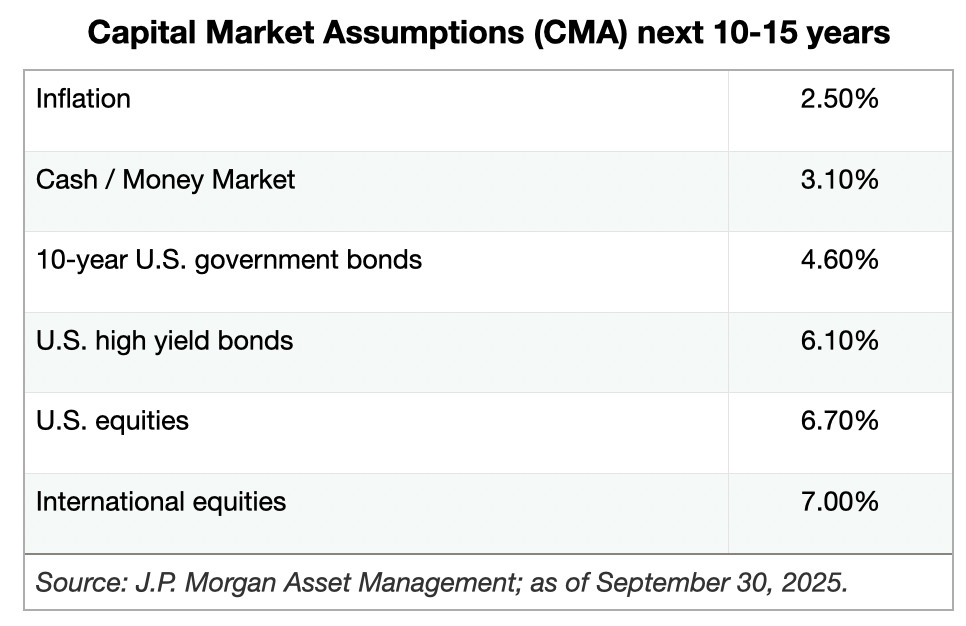

Those are excellent questions and hold significant importance as they play a crucial role in the assumptions we make about the future and retirement calculations. Our forward-looking expected returns for the next ten to fifteen years are provided by J.P. Morgan Asset Management.

Adjusting for inflation, the anticipated real return for the U.S. stock market is approximately 50% lower than its historical average over the past fifty-six years. The historical real return for the past fifty-six years stands at 8.21%, while the expected return for the next ten to fifteen years is 4.2%. Several factors contribute to these lower expectations, but they are acceptable if we can avoid the significant shocks experienced over the past fifty-six years. For instance, on a rolling five-year basis, inflation reached its peak in 1981 at 9.9%, and the stock market recorded its lowest average annual return of -0.77% per year in 1974. This means the stock market had a negative return for five consecutive years! U.S. Treasuries were even more affected, reaching their lowest point in 2025 with a loss of 1.56%.

Fortunately, the fluctuations in inflation, fixed income returns, and the stock market have occurred at varying intervals. This is why strategy is so crucial.

We believe that a strategy refresher every quarter is beneficial because it helps us stay focused on tried and true methods that have proven effective, enabling us to navigate through challenging situations with confidence.

The Erisa Retire Ready investment strategy is straightforward. Over the past 125 years, we’ve observed that if you invest in the stock market for at least ten years, starting from 1900, the returns on a rolling ten-year basis have consistently been positive. This holds true despite significant global events such as two world wars, other conflicts, oil embargoes, high interest rates, and high inflation. The key takeaway is that investment funds should be allocated based on their future needs. If the funds are required within the next five years, it’s advisable to avoid investing in the stock market. However, if the funds are needed within seven, ten years, or more, the stock market offers the highest potential for returns. Essentially, the strategy is to align investments with the timing of when the funds will be needed.

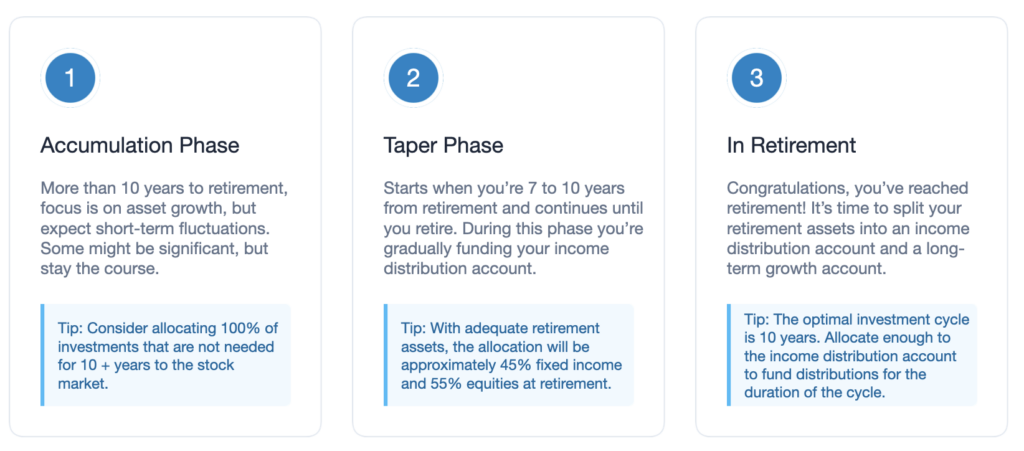

For retirement planning, this can be divided into three phases. The first phase, the accumulation phase, spans from your entry into the workforce until you’re approximately ten years away from retirement. The second phase commences when you’re about ten years from retirement and continues until retirement itself. The third phase is retirement, when your accumulated retirement funds replace your earned income.

Starting with the taper phase leading up to retirement, the strategy focuses on building a fixed income distribution account that will provide monthly distributions during retirement. All other retirement funds are directed towards a growth strategy, with the expectation that the growth account will significantly outperform inflation over the long term.

In summary, as we reflect on Q1 2026, we observe some similarities with past events. However, some of these similarities are merely distractions that can divert our attention from the fundamental principles of investing. The most basic principle is to align your investments with the timing of future fund requirements. Perhaps it’s time to put on noise-canceling headphones and pick up some Dramamine.

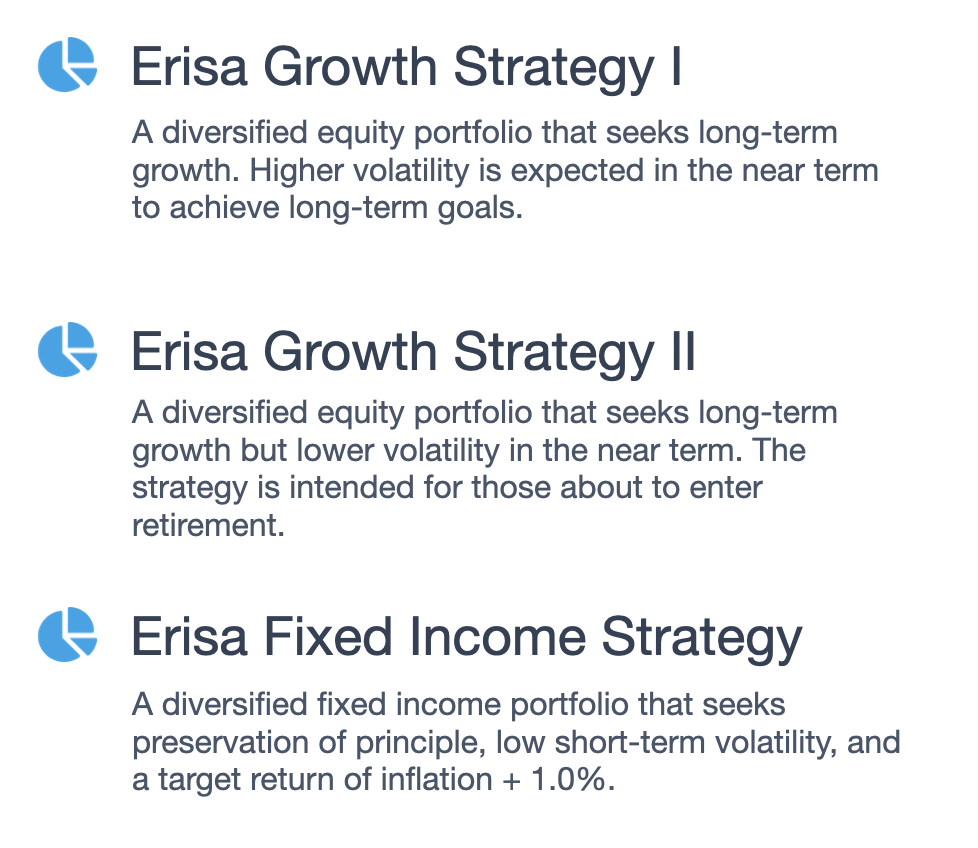

Erisa RetireReady Investment Strategy

Erisa investment portfolios for each phase to and through retirement

Disclaimer: The Erisa Market Quarterly, published by Erisa Advisers, Inc., an SEC-registered investment advisory firm, provides insights into the market. However, it’s important to note that investment returns are not guaranteed. Given the diverse needs and circumstances of each investor, seeking professional advice before making investment decisions is highly recommended.